What Is Telematic Insurance?

Telematic insurance is a modern approach to vehicle insurance that customizes premiums based on the driver’s real-time behavior and vehicle usage. Utilizing telematics technology, this insurance model involves placing a device in the vehicle or employing a smartphone app to monitor various driving metrics. These metrics typically include speed, acceleration, braking intensity, distance traveled, time of day, and driving routes.

By analyzing this data, insurance companies can create a risk profile customized to the individual driver, leading to more accurate premium calculations. Safe drivers who maintain consistent speeds, avoid harsh braking, and drive during less risky times are often rewarded with reduced premiums. Conversely, those who frequently engage in high-risk driving behaviors might face higher insurance costs.

This approach not only offers a fairer pricing model but also encourages safer driving habits, making telematic insurance a growing trend in the automotive insurance industry.

Key Features Of Telematics Insurance

Telematics insurance utilizes advanced technology to provide a detailed assessment of driving behaviors, influencing insurance premiums based on individual driving patterns. Here are the essential features of this insurance type:

- GPS Tracking: Utilizes GPS to monitor vehicle location, speed, and route choices. This data helps insurers assess driving patterns and adjust premiums accordingly.

- Acceleration and Braking Monitoring: Tracks how smoothly or aggressively a driver accelerates and brakes, offering insights into safe or risky driving habits.

- Mileage Tracking: Records the total distance driven, allowing insurers to adjust premiums based on vehicle usage. Lower mileage can lead to lower insurance costs.

- Time-of-Day Tracking: BMonitors when the vehicle is driven. Driving during high-risk times, such as late at night or during rush hours, can impact the premium.

- Cornering and Steering Analysis: Evaluates how turns and steering are handled. This feature reflects driving style and overall vehicle control.

- Phone Usage Monitoring: Some telematics devices can track phone use while driving, helping to reduce distractions and encourage safer driving practices.

- Eco-Driving Analysis: Assesses driving habits to promote fuel efficiency and reduce emissions, which can be beneficial for both the driver and the environment.

- Real-Time Feedback: Provides insights into driving habits through a mobile app or online portal and helps drivers improve their driving behavior.

Key Market Takeaway For Telematics Insurance

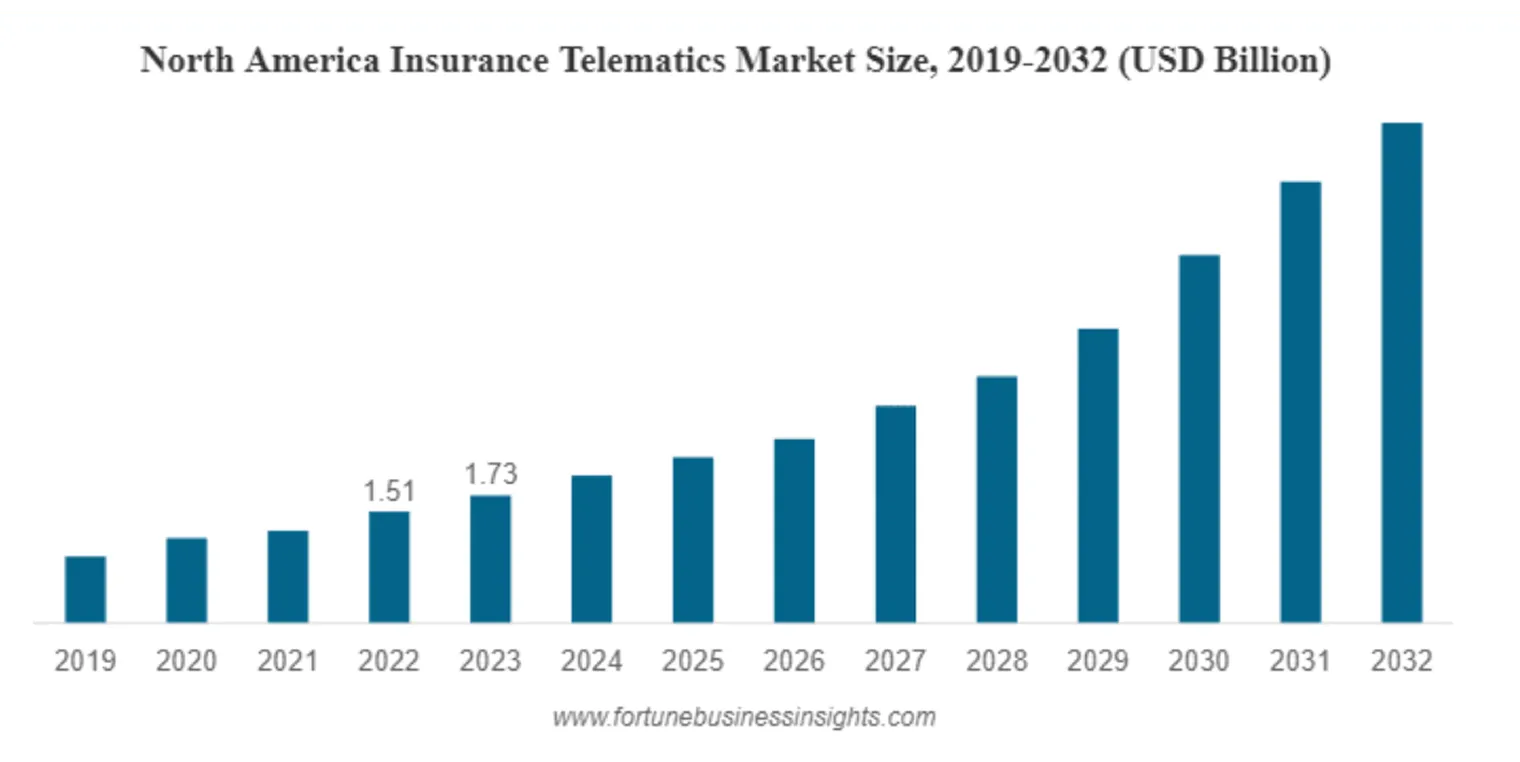

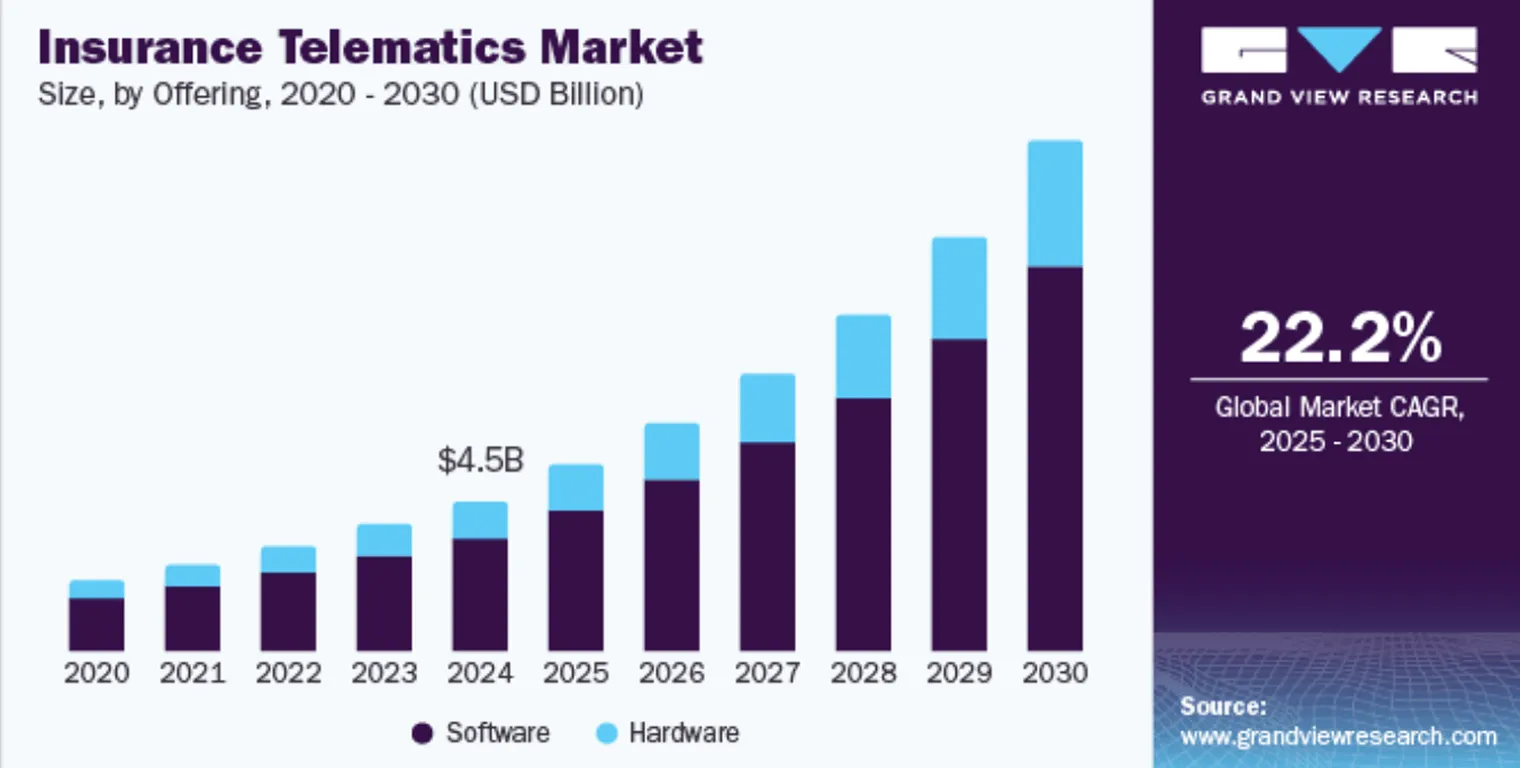

The global insurance telematics market was valued at $4.33 billion in 2023. It is anticipated to grow from $5.03 billion in 2024 to $19.23 billion by 2032. This represents a compound annual growth rate (CAGR) of 18.2% throughout the forecast period.

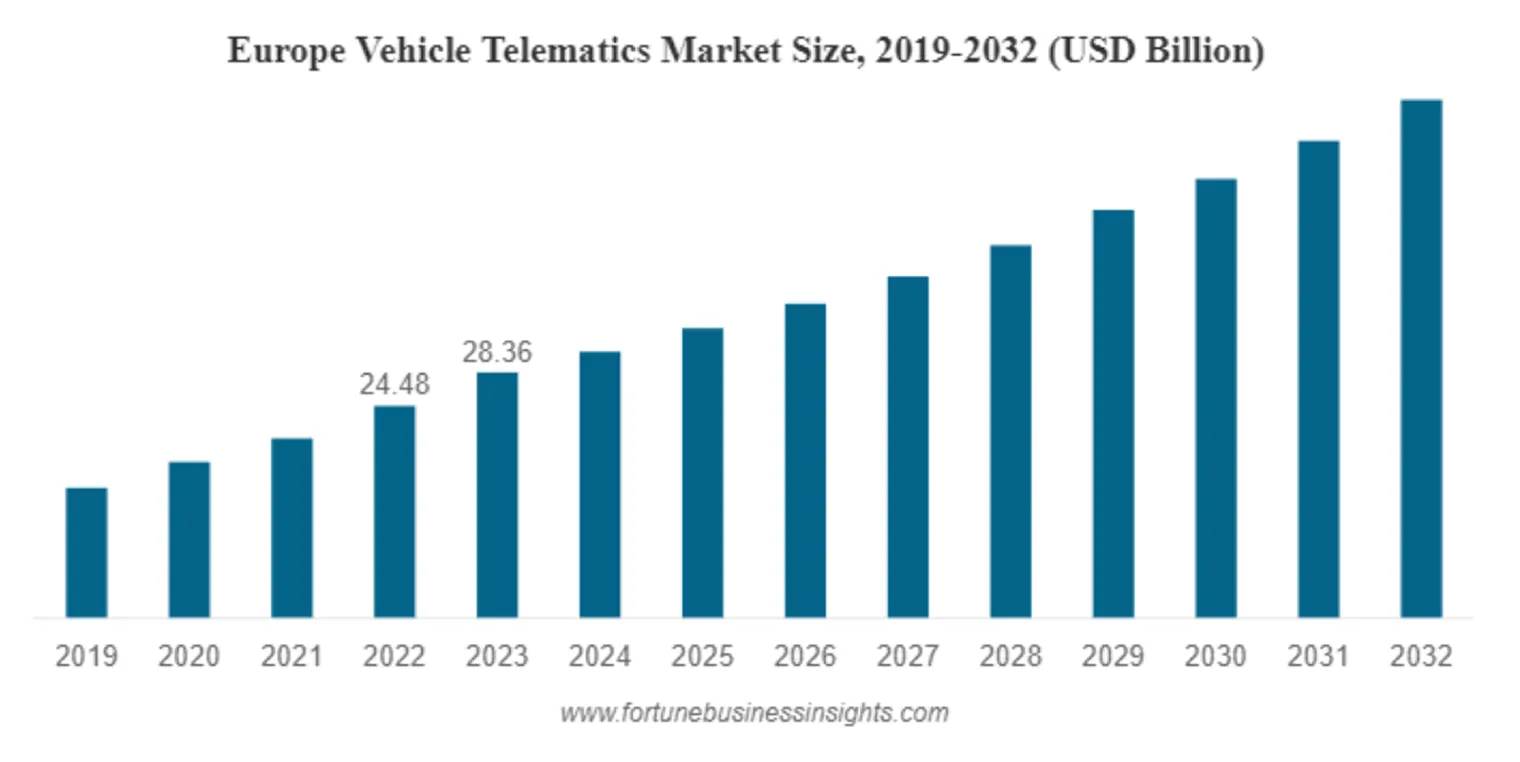

Similarly, the vehicle telematics market had a valuation of $79.17 billion in 2023. Projections indicate it will rise from $85.95 billion in 2024 to $170.35 billion by 2032, with a CAGR of 8.9%. This growth is driven by the increasing adoption of telematics systems by automotive manufacturers for both passenger and commercial vehicles. Additionally, heightened consumer awareness about the benefits of telematics - such as improved vehicle performance insights and driver behavior analysis - is encouraging fleet operators and vehicle managers to implement these systems. The broader adoption of telematics products by original equipment manufacturers (OEMs) and aftermarket providers is also contributing to market growth.

In the telematics-based auto insurance sector, revenue is expected to reach $2,513.9 million in 2023. This market is projected to expand significantly, with a CAGR of 18.7%, potentially reaching $13,998.3 million by 2033. The increasing demand for telematics-based insurance solutions is driven by the rise of connected cars, technological advancements in telematics, and the growing need for personalized insurance options.

Types Of Telematics Insurance

Telematics insurance comes in two primary forms, each leveraging different technologies to monitor driving behavior and adjust premiums accordingly. Here’s a detailed overview:

- Pay-As-You-Drive (PAYD): This type of telematics insurance adjusts your premium based on the total miles you drive. The less you drive, the lower your insurance cost. PAYD is ideal for individuals who use their vehicles infrequently, offering significant savings by aligning costs with actual usage.

- Pay-Per-Mile (PPM): Similar to PAYD, Pay-Per-Mile insurance includes a base rate plus a fee for each mile driven. This model is particularly beneficial for low-mileage drivers, as it directly ties the premium to the distance traveled, making it a flexible option for those with variable driving patterns.

- Behavior-Based Insurance: This model focuses on how you drive rather than how much you drive. By monitoring driving behaviors such as acceleration, braking, speed, and even phone usage while driving, insurers can adjust premiums based on the level of risk associated with your habits. Safe driving behaviors can lead to significant discounts, while riskier behaviors may increase costs.

- Black Box Insurance: Also known as telematics box insurance, this type involves installing a small device (black box) in your vehicle. The black box monitors various aspects of your driving, including speed, mileage, and driving times. This detailed data allows insurers to tailor your premium based on real-time driving conditions and habits.

- Green Insurance: Green insurance rewards drivers who adopt eco-friendly driving habits, such as avoiding rapid acceleration and harsh braking. These behaviors not only reduce fuel consumption but also lower emissions, and insurers may offer discounts for environmentally conscious driving.

How Does Telematic Insurance Work?

Telematic insurance operates through a series of steps designed to customize your auto insurance premium based on your driving behavior. Here’s how the process unfolds:

- Program Enrollment: To begin, you enroll in a telematics-based insurance plan with your provider, consenting to the collection and use of your driving data.

- Technology Integration: Depending on the insurer, you’ll either install a telematics device in your vehicle, download a dedicated smartphone app, or utilize existing in-car telematics systems. These tools are responsible for monitoring your driving habits.

- Data Monitoring: The installed technology continuously captures detailed driving data, including your speed, acceleration, braking patterns, total distance driven, and the times of day you typically drive. In some cases, it also records phone usage while the vehicle is in motion.

- Data Transmission: The captured data is securely transmitted to your insurance provider, either in real-time or at specified intervals.

- Behavioral Analysis: The insurance company analyzes the data to evaluate your driving risk profile. Safe driving habits—such as smooth acceleration and braking, consistent speeds, and driving during low-risk times—can result in a lower risk assessment.

- Premium Calculation: Based on the analysis, your insurance premium is dynamically adjusted. This adjustment can occur on a monthly, quarterly, or yearly basis, reflecting your actual driving behavior.

- Driving Insights: Many insurers offer personalized feedback through an app or online portal, allowing you to review your driving patterns and receive tips for improvement. Consistent, safe driving can lead to further discounts and incentives.

Traditional vs. Telematics Insurance: A Comparison

Telematic insurance operates through a series of steps designed to customize your auto insurance premium based on your driving behavior. Here’s how the process unfolds:

- Premium Calculation: Traditional Insurance bases its premiums on general factors like the driver’s age, gender, location, vehicle type, driving history, and credit score. These elements are combined with statistical models to estimate the overall risk, resulting in a fixed premium that typically remains constant throughout the policy period.

Telematics Insurance, on the other hand, uses real-time data to calculate premiums. It closely monitors specific driving behaviors such as speed, acceleration, braking, mileage, and driving times. This approach allows for a more personalized premium that can fluctuate depending on how safely you drive, potentially offering significant savings for cautious drivers. - Risk Assessment: Traditional Insurance bases its premiums on general factors like the driver’s age, gender, location, vehicle type, driving history, and credit score. These elements are combined with statistical models to estimate the overall risk, resulting in a fixed premium that typically remains constant throughout the policy period.

Telematics Insurance provides a more precise risk assessment by focusing on real-time driving behaviors. By tracking and analyzing how you drive, it adjusts your premium according to your actual risk level. This method rewards safe driving practices and can result in lower premiums for those who consistently demonstrate low-risk behaviors. - Premium Flexibility: With Traditional Insurance, premiums are typically fixed for the duration of the policy. Changes in premiums generally occur only at renewal, based on updated information or changes in the insured’s circumstances.

In contrast, Telematics Insurance offers greater flexibility. Since premiums are adjusted based on ongoing monitoring of driving behavior, safe driving can lead to lower premiums over time. Conversely, risky behaviors may result in higher costs, providing continuous incentives for safe driving. - Discounts And Rewards: Traditional Insurance offers discounts based on broad criteria, such as maintaining a clean driving record, bundling multiple policies, or having safety features in the vehicle. These discounts are predetermined and apply to a wide range of drivers.

Telematics Insurance takes discounts a step further by offering rewards based on real-time driving data. Safe drivers receive immediate feedback through apps or online portals, which can help them improve their driving habits. Over time, these improvements can lead to more substantial discounts and a more customized insurance experience. - Technology And Monitoring: Traditional Insurance does not involve active monitoring of driving behavior. The premium remains unaffected by how the insured drives during the policy period.

Telematics Insurance integrates technology into the driving experience, using devices like plug-in modules, mobile apps, or built-in car systems to monitor driving habits continuously. This technology-driven approach not only provides insurers with accurate data but also empowers drivers with actionable insights into their driving patterns.

| Aspect | Traditional Insurance | Telematics Insurance |

|---|---|---|

| Premium Calculation | Fixed, based on demographics and vehicle factors. | Variable, based on real-time driving behavior. |

| Risk Assessment | General, based on statistical data and demographics. | Detailed, based on actual driving data. |

| Premium Flexibility | Fixed for the policy period, adjusted only at renewal. | Adjusted regularly based on driving habits. |

| Discounts and Rewards | General discounts for safe driving, bundling, or features. | Personalized discounts for specific driving behaviors. |

| Technology and Monitoring | No real-time monitoring. | Continuous monitoring via devices or apps. |

Benefits Of Telematics Insurance

Telematics insurance presents several significant advantages for both drivers and insurance companies. Here’s a detailed look at its benefits:

Advantages For Policyholders

- Potential for Lower Premiums: Drivers who exhibit safe and efficient driving behaviors can enjoy substantial savings on their insurance premiums. Discounts of up to 40% are possible for those who consistently demonstrate responsible driving.

- Customized Premiums: Unlike traditional policies, telematics insurance bases premiums on actual driving habits. This personalization ensures that the cost of insurance more accurately reflects individual driving behavior.

- Enhanced Driving Insights: Policyholders receive detailed feedback on their driving patterns. This real-time information helps individuals identify areas for improvement, which can lead to further premium reductions.

- Environmental Benefits: The system promotes eco-friendly driving by rewarding behaviors that reduce fuel consumption and lower emissions, contributing to a greener environment.

Advantages For Insurers

- Precise Risk Evaluation: Insurers benefit from detailed, real-time data that enhances the accuracy of risk assessments. This allows for a more precise and fair premium setting.

- Fraud Prevention: By analyzing comprehensive driving data, insurers can detect patterns indicative of fraudulent claims, thereby reducing fraud and associated costs.

- Enhanced Customer Interaction: The technology provides a platform for continuous customer engagement through personalized feedback and educational resources, improving overall customer satisfaction.

- Reduction In Claims Frequency: Encouraging safe driving habits through telematics can lead to a decrease in accidents and claims, which benefits insurers by reducing overall claim expenses.

Current Adoption and Market Trends

Adoption rates are rising, with a TransUnion survey reporting a 33% increase in customers accepting telematics offers since late 2021, and 30% of non-users expressing high interest (EasySend on Telematics). The North American insurance telematics market is estimated at 105.81 million active premiums in 2025, expected to reach 379.45 million by 2030 at a CAGR of 29.1%, driven by connected vehicles, with over 400 million projected on the road by 2025 (North America Insurance Telematics Market). This growth is fueled by technological advancements like AI, IoT, and 5G, enhancing user experience and data monetization (Insurance Telematics Market Report).

Challenges Of Insurance-Based Telematics

Telematics-based insurance solutions offer numerous benefits, but they also come with specific challenges. Here’s a clear overview of these issues:

- Data Privacy And Security: Protecting customer data is a fundamental concern. Insurance companies must comply with regulations like GDPR to ensure data privacy. This involves using strong encryption and secure storage methods to prevent unauthorized access and breaches. Without these measures, sensitive information could be at risk.

- Technological Compatibility: Telematics systems must operate across various devices and operating systems. Developing solutions that work seamlessly on different platforms can be complex. Additionally, analyzing large volumes of data requires advanced computational tools. Ensuring that data from multiple sources is standardized and accurate is also vital for reliable analysis.

- Network Coverage and Connectivity: Stable network connections are essential for real-time data transmission. However, poor network coverage or unstable connections can disrupt this process, affecting the accuracy and timeliness of the data collected. To mitigate this, investing in technologies that enhance connectivity or using systems designed for low-connectivity areas can be beneficial.

- Cost And Return on Investment (ROI): The initial investment in telematics technology can be substantial, including costs for devices, software, and infrastructure. Demonstrating a clear return on investment can be challenging, particularly in the early stages. Insurance companies need to evaluate how telematics improves risk management and customer retention to justify these costs.

- Data Quality And Accuracy: Ensuring accurate data is essential for assessing risk and setting prices correctly. Issues such as incorrect readings or anomalies must be addressed through effective data processing techniques. Implementing data verification and cleansing processes helps maintain data integrity.

- Scalability: As the user base for telematics solutions grows, so does the volume of data and the need for processing power. It’s important for insurers to ensure that their systems can handle increased demands without sacrificing performance. Investing in scalable infrastructure and optimizing data workflows is key to managing this growth effectively.

Conclusion

Telematics technology is changing the insurance industry by offering a more accurate and fair way to assess risk and set premiums. By using real-time data on driving habits, telematics allows insurers to adjust premiums based on individual driving patterns. This approach rewards safe drivers with lower costs and promotes better driving habits. As telematics adoption grows, driven by advances in connectivity and data analysis, it is addressing many inefficiencies found in older insurance models. The continued development of telematics is set to improve customer satisfaction and operational efficiency, leading to more personalized and fair insurance options.